Authors

.avif)

Contents

Find out how we can help you navigate environmental markets

As the world progresses towards net zero, some businesses have a harder time reducing their emissions. In this article, we will discuss why it is more challenging for certain businesses to abate their emissions, and we will discuss why carbon offsets can play a key role in addressing the decarbonisation of hard-to-abate sectors.

Hard-to-abate emissions

Hard-to-abate emissions are emissions that are either prohibitively costly or impossible to reduce with currently available abatement technology. These emissions usually occur in one of two categories: heavy industry (e.g. cement, steel, and chemicals manufacture), and heavy-duty transport (e.g. trucking, shipping, and aviation). Hard-to-abate sectors contribute to approximately 30% of global emissions, and this share is expected to double under business-as-usual scenarios.

For the rest of the economy, the path to net zero is relatively straightforward: some combination of energy efficiency and switching to carbon-free energy sources. The transition for the hard-to-abate sectors is not so straightforward. A lot of promising abatement technologies exist but most of them are prohibitively expensive or not mature enough to play a significant role in reducing carbon emissions right now.

Achieving economies of scale and reduction in development costs mean that abatement technologies become commercially viable and are gradually phased in. The problem is that this pace does not match the urgency required of us to stay on track for the Paris Agreement emissions goals.

Abatement challenges

For heavy-duty transportation (trucking, shipping, and aviation), we do not yet have a commercially viable way to compete with the density and portability of fossil fuels. Unless there is a major breakthrough in battery density or in alternative fuels, long-haul shipping precludes the use of electric vehicles. The most promising alternative fuel sources – hydrogen, biofuels, and synfuels – require substantial process re-design and are not yet produced at scale.

In heavy industry (cement, steel, and chemicals), fossil fuels remain the cheapest option for many unavoidable industrial processes. Take industrial heat as an example. Industrial heat is the extremely high heat needed to produce steel, cement, and some chemicals. Around 10% of global CO2 emissions come from the combustion required to produce this high-temperature heat. Fossil fuels remain the best option for cheaply producing it at scale.

Fossil fuels are also a vital chemical input for a lot of heavy industry. For example, consider the obvious dependence that petrochemicals like plastics and synthetic rubber have on fossil fuels for their creation. Or how steel production uses coke (a type of coal with high-carbon content) for its unique chemical structure, and replacing coke with an alternative material is not practical.

Another challenge is that heavy industry and heavy-duty transport have long asset lives. Industrial plants and equipment take decades to naturally phase out, so it is hard to convince companies to immediately switch to new technologies.

Promising innovations

Improvements will likely be made in battery density to allow for lighter batteries with longer charges. This, along with advancements in hydrogen production and storage solutions, as well as increased commercial viability of alternative fuel sources, may enable heavy-duty transportation sectors to significantly decarbonise.

The biggest reductions in heavy industry emissions will come from greater recycling and reuse, energy efficiency, hydrogen as a heat source, and direct electrification of production processes.

Carbon offsets can help cover the 'green premium' and accelerate adoption of cleaner solutions.

Much of the technologies that will eventually help reduce emissions from hard-to-abate sectors are far from being commercially viable today. Goldman Sachs’ Carbonomics research estimates that ca. 25% of global GHG emissions are un-abatable under current technologies at prices of <$1000 per tonne of CO2 equivalent. This is partially true because we do not factor the true economic and environmental costs or negative externalities resulting from existing energy options into the price we pay for them. The 'Green Premium' is a concept brought to life in the recent Bill Gates book which describes the additional cost of adopting a clean technology over one that emits a greater amount of greenhouse gases.

To allow decarbonisation at scale, the green premiums would need to be low enough for producers or manufacturers to choose the clean alternative over the higher emissions.

Voluntary carbon offsets can be a way for corporations wanting to accelerate the decarbonisation in hard-to-abate sectors to subsidise part of the 'Green Premium'. This approach also allows hard-to-abate sectors – which are often being regulated under a compliance carbon market or carbon tax regime – to lower their carbon footprint and the resulting carbon liabilities, ultimately driving to a potential carbon tax savings for them - a true 'win-win' solution for all parties.

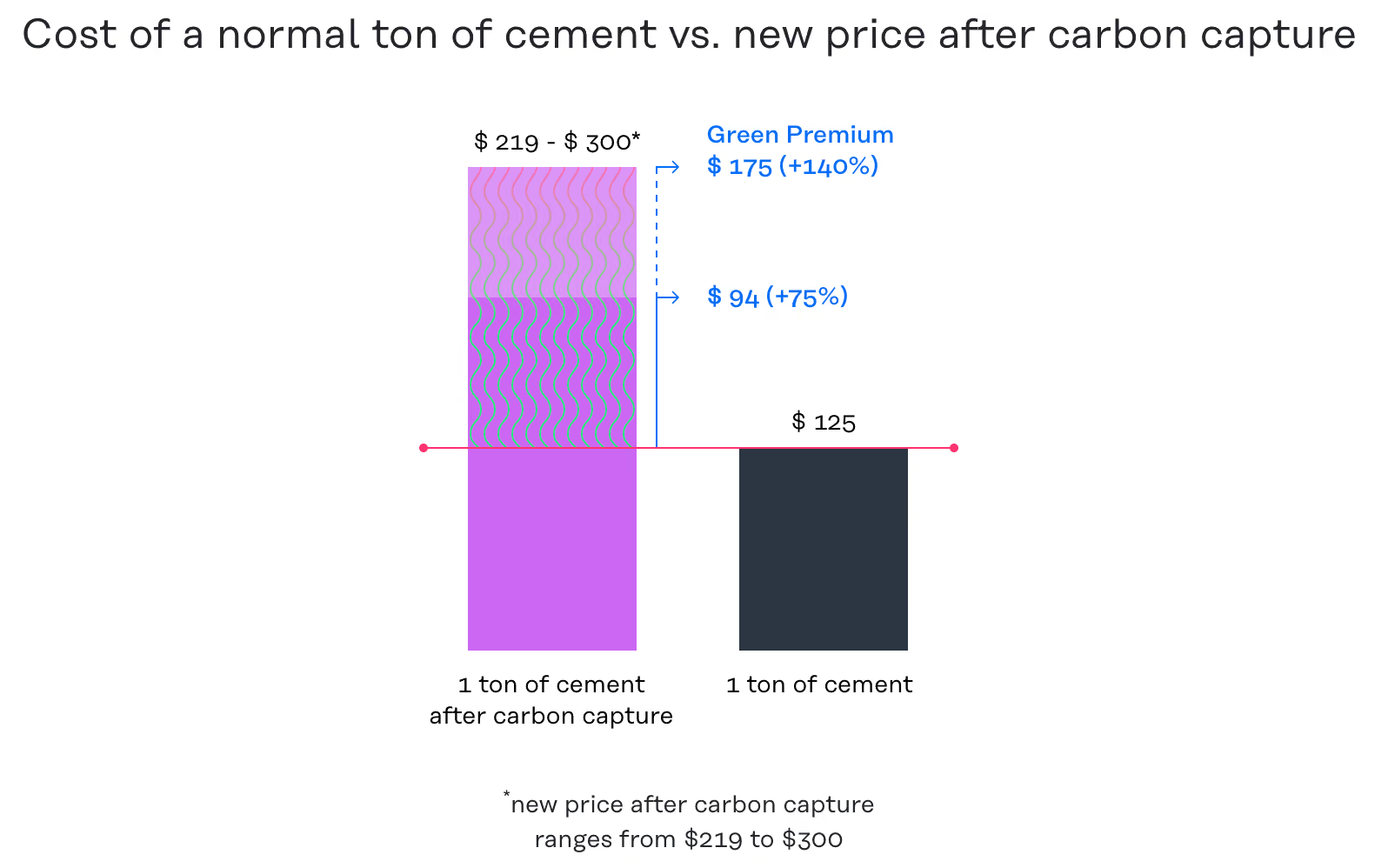

Let’s take the example of cement production. It costs between $219-300 for a tonne of 'clean' cement (where CO2 is captured and sequestered in the cement production) against $125 for a tonne of conventional cement. Cleaner cement production is between 75% to 140% more expensive relative to conventional. Carbon credits with a price of or less than $94-175 per tonne of cement purchased by corporations as part of their offsetting budgets could be providing the right incentive to compensate cement manufacturers and have them start adopting cleaner cement solutions in their production phase. A carbon price of up to €131/mt will be necessary for some technologies, such as carbon capture and storage, that are likely needed for most emissions cuts from the cement sector, according to a 2021 report from German thinktank Agora Energiewende.

For net-zero ambitions to be realised, offsets will ultimately need to generate negative emissions, i.e., remove emissions rather than merely reduce them. Demand for voluntary carbon offsets has started to be focused on offsets from companies that have developed carbon removal solutions (e.g. CO2 utilisation in cement production, Direct Air Capture coupled with geological storage (DACCS) or even biochar production for the horticulture sector that sequesters carbon in top soils). Voluntary carbon offsetting programs can directly contribute to directing resources for R&D budgets and support the development of these removal pathways at scale.

Together with policy interventions, carbon credits have the potential to be an effective instrument in accelerating decarbonisation action in the hard-to-abate sectors.

About Abatable

We started Abatable for exactly this reason - to help companies offset their hard-to-abate emissions. We enable carbon procurement and climate contributions at scale by giving organisations the access and tools to navigate the complex carbon markets. We focus our efforts on providing corporations with access to high-quality carbon offsets scored on proprietary framework to assess the quality of both the carbon project and the carbon project developers. We guide corporate climate action towards projects which have proven ability to decarbonise industries at scale or play a key role in climate mitigation activities.

If you’re with a company operating in one of these hard-to-abate sectors, get in touch.