Authors

Contents

Find out how we can help you navigate environmental markets

Abatable’s Holly Nicholson explains what SBTI’s CNZS V2 means for company climate and carbon market strategies.

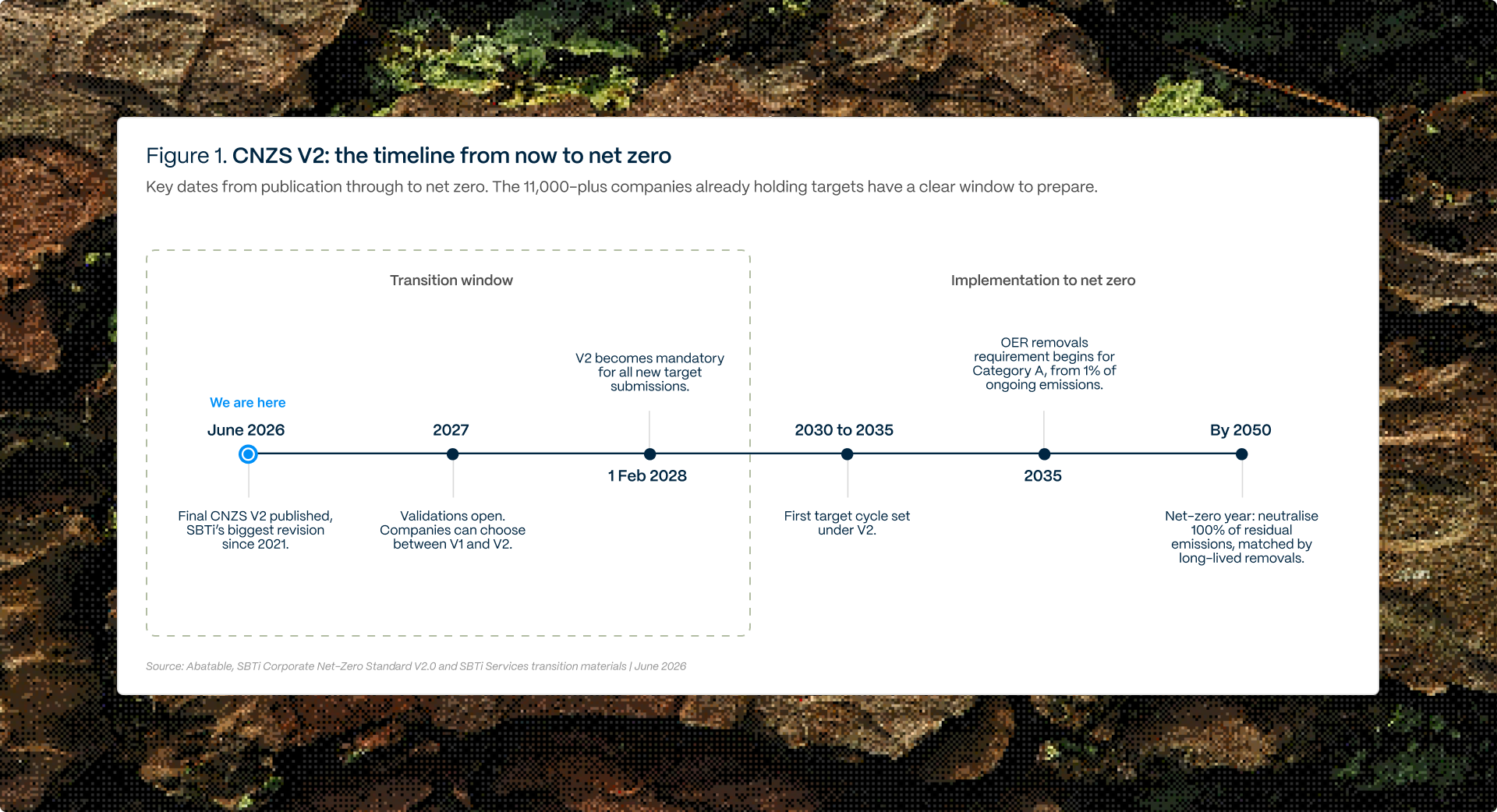

The Science Based Targets initiative (SBTi) has published the final version of its long-awaited Corporate Net-Zero Standard Verson 2.0 (CNZS V2), its most significant revision to its flagship net-zero standard since 2021.

Companies can choose to be validated under the new standard in 2027, and it will become mandatory for new company submissions from 1 February 2028. Existing targets remain valid until the end of their five-year cycle, so the 11,000-plus companies already holding targets have a clear window to prepare.

If you are considering how to take action on your emissions on the route to net zero, plan for carbon removal credit use, or are weighing up commodity certificates and how to use them, here’s what matters most about the new SBTi guidance rules.

Key takeaways

- For the first time, companies that take responsibility for their ongoing emissions as they transition to net zero can be formally recognised for it, through SBTi’s new Ongoing Emissions Responsibility (OER) framework.

- From an accounting perspective, carbon credits, what the standard calls ‘verified mitigation outcomes’, sit alongside your Scope 1, Scope 2, and Scope 3 targets – they don’t count towards emissions reduction targets – but OER now gives them a structured, recognised role.

- From 2035, Category A companies – large companies or medium-sized companies in high-income countries – must purchase carbon removal credits, starting at 1% of ongoing emissions and rising to 100% of residual emissions by their net-zero year.

- What SBTi terms ‘market instruments’, including commodity and energy certificates, can now support target implementation across all three scopes, as long as they are reported separately from your emissions inventory.

- If you miss an emissions target, SBTi now recommends you voluntarily buy carbon removals to cover the shortfall.

What V2 actually changes

CNZS V2 sees SBTi pivoting from helping companies set targets to actually implementing them. As the document’s foreword puts it: commitment is not the hardest part, delivery is.

Under CNZS V2, companies now have more flexible ways to set targets based on the nature of the company: Scope 1 has three near-term routes based on absolute emissions, emissions intensity or asset transition; Scope 2 adds a low-carbon electricity option, and the previously rigid Scope 3 coverage thresholds (67% near-term and 90% long-term reductions) give way to a significance test. Scope 3 targets include every category worth 5% or more of your value chain footprint, with named exceptions, such as employee commuting and some franchise and downstream emissions, that you can leave out even above that line. CNZS V2 also makes board-level governance and a transition plan conditions of validation.

Your physical greenhouse gas inventory will determine the majority of target progress, though with more nuance by allowing activities undertaken at the activity pool or sector level (which may not show up in the inventory) to count towards your target. What is new for anyone buying carbon credits, carbon removals, or other market instruments is that these now have defined, separately reported roles across all three scopes, rather than sitting on the margins.

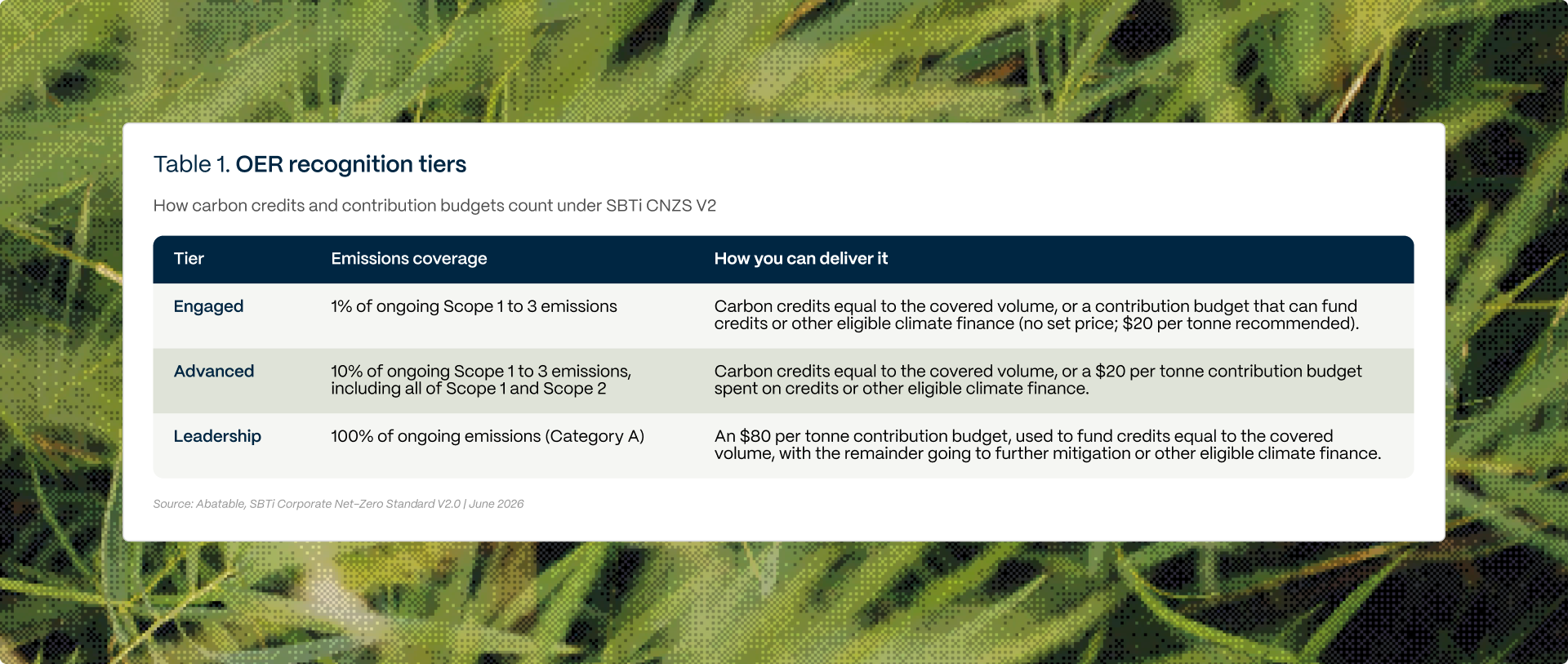

Carbon credits and the new recognition tiers

The headline for carbon credit buyers under CNZS V2 is recognition. For the first time, SBTi is rewarding companies that take responsibility for their ongoing emissions as they transition to net zero, through Ongoing Emissions Responsibility (OER). From 2035, it requires Category A companies – large companies or medium-sized companies in high-income countries – to use carbon removals while they keep cutting emissions.

Credits still do not substitute for reductions, which must come from your own value chain, but they now have a clear home rather than the loosely defined ‘beyond value chain mitigation’ of CNZS V1.

OER’s voluntary recognition programme arrives with V2, so you can engage with it as you move onto the new standard from 2027. It has three tiers (see Table 1) that reflect the level of ambition undertaken, and carbon credits, which the standard calls ‘verified mitigation outcomes’, are an eligible way to deliver at each one.

The ‘Advanced’ tier is a new addition from the consultation draft. You can cover its 10% in two ways: retire carbon credits equal to that volume, or commit to a $20-per-tonne ‘contribution budget’. That budget is a financing commitment you can spend on carbon credits or direct to other eligible climate finance, such as future carbon removals, conservation and nature finance, or research and adaptation, provided you commit it within the five-year period it covers. Either route gives you a defensible anchor for internal carbon pricing.

Under OER companies can demonstrate they are taking additional climate responsibility as they move towards net zero. Whatever tier you choose, the credits you support have to clear a defined integrity bar: there needs to be documented due diligence covering additionality, leakage adjustment, reversal protection, and independent assurance. SBTi will recognise existing third-party integrity frameworks rather than build its own (they are conducting further work on which specific standards will be endorsed), so knowing which credits actually clear the bar falls to you and your procurement partners.

Removals: the requirement that arrives in 2035

OER also sets out when removals stop being optional. From 2035, Category A companies must support eligible carbon removals equal to at least 1% of their ongoing Scope 1–3 emissions, rising in a straight line to 100% by their net-zero year and no later than 2050, with a growing share coming from durable, long-lived removals.

At the net zero year itself, residual long-lived emissions must be neutralised with long-lived removals. SBTi is set to open a Call for Evidence on whether shorter-lived removals can ever qualify, so expect the rules here to evolve slightly.

There is also a new addition to the standard, even when you are broadly on track: if you miss a target, SBTi now recommends you voluntarily purchase carbon removals to cover the shortfall. These do not count towards progress and must meet the same integrity criteria, but the overall message is clear: a credible climate strategy now plans for investing in carbon removal well before 2050. Given likely supply constraints in durable storage, the companies mapping that curve now will be best placed.

Insetting: which side of the line?

Insetting sits on the value chain side of all this. A reduction or removal you achieve inside your own supply chain counts towards your target through your inventory, provided you don’t transfer it. Issue it as a credit and sell it, and it leaves your target accounting to become an OER activity instead. If you run a credit-based insetting programme today, you will need to decide which side of that line each project belongs on.

Market instruments for value chain action

For value chain emissions you cannot yet cut directly, market instruments are the tool to help in CNZS V2. Commodity certificates – think for green steel, low-carbon fertiliser, or sustainable aviation fuel – let you show progress against a Scope 3 target, while energy contracts and certificates do the same for Scope 2.

These instruments have to meet consistent integrity rules. They must:

- match the same product or energy source in your inventory;

- cannot exceed the volume you actually report;

- sit within roughly 12 months of the activity you are addressing with the instrument; and

- come through a secure registry from a programme that drives change at the system level.

You report them separately from your emissions inventory, in line with the Greenhouse Gas Protocol’s emerging multi-statement approach, with further SBTi guidance on this expected for consultation in late 2026. One rule matters for carbon project developers: the same activity cannot issue both a carbon credit and a commodity certificate, so instrument choice is now a real strategic decision.

What this means for you

CNZS V2 sorts companies into two categories by size and footprint.

If you’re a Category A company – a larger businesses or medium-sized business in a high-income countries – you carry the full obligations, including the post-2035 removals requirement and third-party assurance, so your removals and OER planning can sensibly start now.

If you’re a Category B company – a medium-sized company in a middle- and lower-income country – the requirements are lighter and carbon removals are optional post-2035. However the the strategic questions – where credits, removals, and market instruments fit – are the same.

Now is the time to prepare: validations open in 2027 and V2 becomes mandatory for new submissions from 1 February 2028 (see Figure 1). Companies with existing targets do not yet need to revisit until their mandatory five-year revalidation cycle is triggered, with the next target cycle running 2030 to 2035.

How we can help: Abatable works with companies on exactly these questions: due diligence so your OER credits stand up to scrutiny, procurement across the recognition tiers, a removals strategy for the post-2035 ramp, and insetting and market instrument programme design. If you are working out what V2 means for your climate and environmental asset strategy, get in touch.